Mortgage Stress Surges to 26.8 Percent After Three RBA Rate Hikes What Brokers Must Do Now

In this guide

- The Numbers: From Three-Year Low to Rapid Reversal

- Arrears Data: The Cracks Are Showing in Different Places

- The Repayment Priority Shift: Mortgages Are No Longer Sacred

- Demand Is Still Climbing — And That Creates Its Own Risk

- Identifying At-Risk Clients Before They Self-Identify

- Refinancing Strategies in a Tighter Market

- Hardship Pathways: Know the Options Before Your Clients Need Them

- Responsible Lending in a Stress Environment

- Client Retention Through Proactive Value

The Numbers: From Three-Year Low to Rapid Reversal

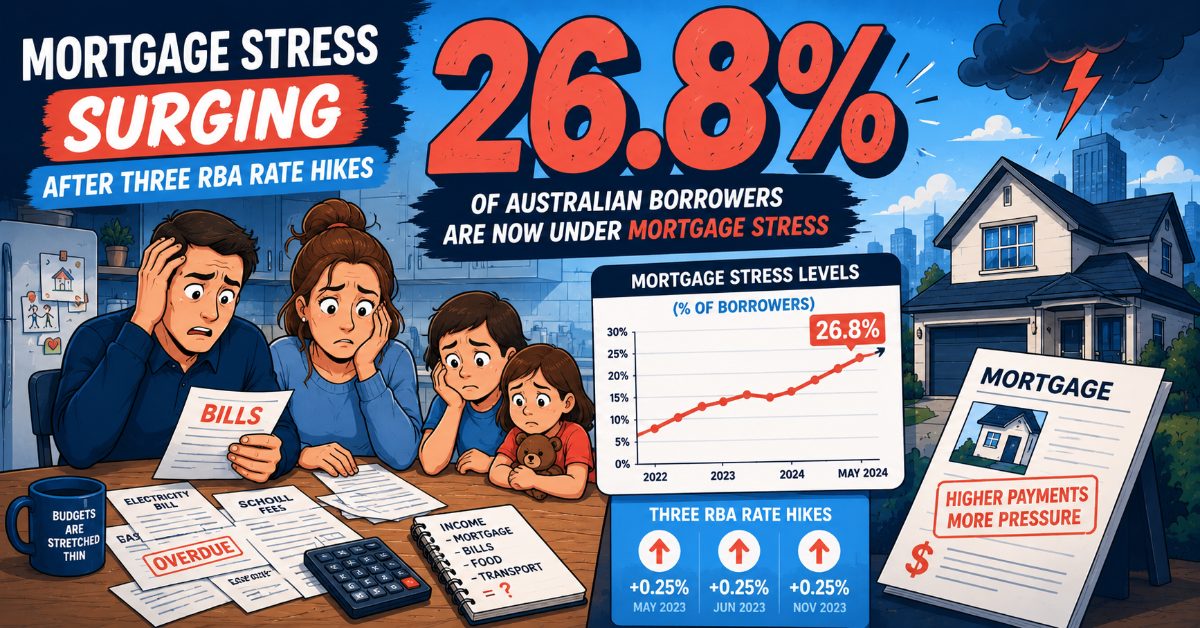

In January 2026, mortgage stress in Australia dropped to its lowest point in three years. Borrowers who had weathered the post-pandemic tightening cycle were finally finding their footing. Then the RBA moved — not once, but three times in quick succession.

Rate hikes in February, March and May 2026 pushed the cash rate to 4.35%, and the effects on household budgets have been immediate. According to Roy Morgan’s latest research, 26.8% of mortgage holders are now classified as being at risk of mortgage stress, up from 23.9% before the February increase. That 1.9 percentage point jump in a single month represents roughly 94,000 additional households tipping into the stress zone.

To put that in raw terms: 1.319 million Australians with a mortgage are now spending more than a quarter of their after-tax income on repayments. Many are spending significantly more than that.

Why It Matters

The speed of the reversal is what matters most for brokers. Clients who appeared comfortably within serviceability buffers at the start of the year may already be stretched. The households most vulnerable are those with variable-rate loans, high loan-to-value ratios, or limited savings buffers — profiles that every broker will recognise in their own book.

Arrears Data: The Cracks Are Showing in Different Places

Equifax’s Q1 2026 Consumer Credit Demand Index adds a critical layer of nuance. The headline figure looks reassuring at first glance: mortgage arrears at 90 days or more actually edged slightly lower during the quarter. But the early-stage indicators tell a different story.

Conforming mortgage arrears at 30 days or more rose 23 basis points to 1.36%. More concerning, non-conforming mortgage arrears at 30 days or more climbed 39 basis points to 5.32%. That non-conforming increase is nearly three times the typical seasonal Q1 rise of approximately 8 basis points.

Key Concept

What does this mean in practice? Borrowers are not yet falling off a cliff in large numbers, but far more are missing early payments or falling behind by a month. The 90-day-plus figure remaining stable reflects the reality that lenders and hardship teams are actively working with distressed borrowers, and that many households are making extraordinary efforts to stay current. But the 30-day data shows the incoming pressure wave.

For brokers managing non-conforming clients — those with prior credit impairment, self-employed borrowers with variable income, or customers who came through specialist lending channels — the 39 basis point jump should trigger immediate portfolio reviews.

The Repayment Priority Shift: Mortgages Are No Longer Sacred

Perhaps the most significant finding from recent data is one that challenges long-held assumptions about borrower behaviour. Experian’s Q1 2026 analysis reveals that mortgages are no longer consistently the number one repayment priority for Australian households.

Historically, the mortgage was the last thing borrowers would let slip. The family home carried both financial and emotional weight that placed it firmly at the top of the payment hierarchy. Borrowers would fall behind on credit cards, personal loans and utility bills before missing a mortgage payment.

That pattern is fracturing. As the cumulative weight of rate rises, cost-of-living pressures and stagnant real wages bears down on households, some borrowers are making different choices. They are protecting their mortgage payments but falling behind on other debts — car loans, personal credit, buy-now-pay-later facilities and credit cards. Others are beginning to let mortgage payments slip while keeping other essentials current.

Key Concept

This shift has profound implications for brokers. A client who appears to be meeting their mortgage obligations on time may nonetheless be in serious financial distress, with mounting arrears across other products. When those secondary debts reach critical mass, the mortgage itself becomes vulnerable. Brokers relying solely on mortgage payment history as a proxy for client wellbeing are likely missing the early warning signs.

Demand Is Still Climbing — And That Creates Its Own Risk

Counterintuitively, mortgage demand rose during Q1 2026 according to Equifax data. Despite the stress signals, Australians are still applying for home loans in growing numbers. First-home buyers are still entering the market. Refinancing activity is elevated. Property investors continue to transact.

Key Concept

This creates a tension that brokers must navigate carefully. On one side, there is genuine business opportunity in a market with rising demand. On the other, there is the obligation — under ASIC’s Best Interest Duty, responsible lending provisions and APRA’s serviceability requirements — to ensure that new lending is genuinely in the borrower’s interest.

The temptation in a rising-demand environment is to focus on volume. The obligation is to focus on suitability. Brokers who get this balance wrong risk poor client outcomes, regulatory scrutiny and reputational damage. Those who get it right will build the kind of client trust that drives referrals and long-term portfolio value.

Identifying At-Risk Clients Before They Self-Identify

The borrowers who call their broker to say they are struggling are already past the early intervention window. The real value a broker adds is in identifying stress signals before the client recognises them — or before they feel comfortable raising the topic.

Practical steps brokers should take now:

- Run a rate sensitivity audit across your loan book. Identify every client on a variable rate or with a fixed rate expiring in the next six to twelve months. Calculate the repayment impact of the current rate environment against what they were paying twelve months ago. Flag anyone whose repayment-to-income ratio has moved above 30%.

- Check buffer positions. Review offset and redraw balances for your client base. Clients who have drawn down their offset or redraw accounts over the past year are depleting their safety margin. A shrinking offset balance is one of the clearest leading indicators of emerging stress.

- Look beyond the mortgage. Where possible, ask clients about their broader financial position. Credit card balances, personal loan commitments and BNPL usage can all signal mounting pressure. Experian’s data makes clear that mortgage-only monitoring is no longer sufficient.

- Monitor communication patterns. Clients who stop responding to annual review invitations, who cancel scheduled check-ins, or who become evasive about their financial position may be avoiding difficult conversations. Silence is often its own signal.

- Segment by risk profile. Non-conforming borrowers, recent fixed-rate expiries, high-LVR loans, single-income households, and borrowers in regions with softening property values all warrant prioritised outreach.

Refinancing Strategies in a Tighter Market

Refinancing remains one of the most powerful tools a broker has for helping stressed clients, but the current environment demands a more nuanced approach than simply shopping for a lower rate.

- Rate negotiation before application. Before submitting a refinance application, approach the existing lender with retention pricing. Many lenders are actively discounting to retain borrowers, and a retention offer avoids the costs, time and credit inquiry impact of a full refinance. In the current market, retention desks are often authorised to offer pricing that matches or beats competitor rates for borrowers with clean payment histories.

- Term extension as a pressure valve. For clients whose primary issue is cash flow rather than total cost of credit, extending the loan term can meaningfully reduce monthly repayments. A borrower 15 years into a 30-year loan who refinances back to a 30-year term will see a significant drop in required payments. This must be discussed transparently — the client needs to understand the trade-off between short-term relief and long-term interest cost — but for households at the edge of stress, it can be the difference between staying afloat and defaulting.

- Product restructuring. Consider whether splitting a loan between fixed and variable portions, consolidating debts into the mortgage (where appropriate and in the client’s interest), or restructuring investment and owner-occupied splits could improve the client’s position. Every option must be assessed against the Best Interest Duty — debt consolidation in particular requires careful analysis to ensure it genuinely benefits the borrower over the life of the arrangement.

- Cashback and offset optimisation. Some lenders are offering cashback incentives on refinances that can help rebuild depleted buffers. Equally, ensuring clients are maximising offset account usage — and that their loan structure supports it — can deliver meaningful savings without requiring a product change.

Hardship Pathways: Know the Options Before Your Clients Need Them

Under the National Credit Code, borrowers experiencing financial hardship have the right to request a variation to their loan contract. Lenders are required to respond to hardship applications within specific timeframes, and ASIC has made clear that it expects lenders to engage genuinely with borrowers in difficulty.

Brokers should be familiar with the hardship provisions available across major lenders, including:

- Temporary repayment reductions — reducing repayments to interest-only or below the minimum contractual amount for a defined period.

- Payment deferrals — pausing repayments entirely for a short period, with the deferred amount capitalised or repaid over the remaining term.

- Loan term extensions — extending the loan term to permanently reduce the required repayment amount.

- Capitalisation of arrears — adding missed payments to the loan balance and re-amortising, which clears the arrears status and resets the repayment schedule.

While brokers cannot submit hardship applications on behalf of clients (this must come directly from the borrower to the lender), they can play a vital role in educating clients about their rights, helping them prepare the necessary documentation, and following up to ensure applications are processed appropriately.

Key Concept

Critically, brokers should normalise these conversations. Borrowers often associate hardship with failure or fear that requesting assistance will damage their credit. Brokers who proactively raise these pathways — framing them as standard risk management tools rather than last resorts — will help clients act earlier and achieve better outcomes.

Responsible Lending in a Stress Environment

APRA’s 3% serviceability buffer remains in place, and for good reason. In the current environment, the buffer is doing exactly what it was designed to do — ensuring that borrowers approved in recent years can absorb some degree of rate increase without immediate distress.

However, the buffer is not a guarantee of comfort. A borrower who was assessed at a 3% buffer above the rate at origination may now be operating at or near that buffer ceiling. Technically serviceable does not mean financially comfortable.

For new lending, brokers must apply particular rigour to household expense verification. ASIC’s responsible lending guidance requires a genuine assessment of the borrower’s financial situation, not just a tick-box exercise. In a market where demand is rising alongside stress, the regulator will be watching for signs that standards are slipping.

Document everything. Record the rationale for why a loan is in the borrower’s interest, particularly where the borrower’s circumstances include any stress indicators. The Best Interest Duty places the obligation squarely on the broker to demonstrate that their recommendation serves the client — not just that the client can technically service the loan.

Client Retention Through Proactive Value

Periods of mortgage stress are when broker-client relationships are either cemented or broken. Borrowers who hear from their broker during difficult times — with practical solutions, not sales pitches — develop the kind of loyalty that no marketing campaign can replicate.

Consider implementing a structured outreach program over the next quarter:

- Week 1-2: Conduct your portfolio risk audit. Identify and segment at-risk clients using the criteria above.

- Week 3-4: Begin direct outreach to the highest-risk segment. Frame the conversation around a routine annual review, not a crisis intervention. Assess each client’s full financial position and identify actionable strategies.

- Week 5-8: Execute on identified strategies — rate negotiations, refinance applications, lender discussions. Follow up on any hardship applications.

- Ongoing: Establish quarterly check-in cycles for all variable-rate and recently-fixed clients. Build this into your CRM workflow so it becomes systematic rather than reactive.

This kind of structured, proactive engagement is what separates transactional brokers from trusted advisers. It is also precisely the kind of evidence that demonstrates compliance with the Best Interest Duty — documented, client-focused, outcome-oriented advice.

The Bottom Line

The surge to 26.8% mortgage stress is not a distant macroeconomic data point. It represents real households in every broker’s portfolio who are under increasing financial pressure. The early-stage arrears data, the shift in repayment priorities, and the speed of the reversal from January’s low all point to a trend that is accelerating rather than stabilising.

Brokers who act now — auditing their books, reaching out to vulnerable clients, preparing refinancing strategies and understanding hardship pathways — will deliver genuine value to their clients while strengthening their own businesses. Those who wait for clients to come to them in crisis will find themselves managing damage rather than preventing it.

The next quarter will be critical. The RBA’s trajectory remains uncertain, cost-of-living pressures show no sign of easing, and the households sitting just above the stress threshold are one unexpected expense away from tipping over. For brokers, the time to act is not when that happens. It is right now.

Strengthen Your Client Relationships Today

{kind=link}