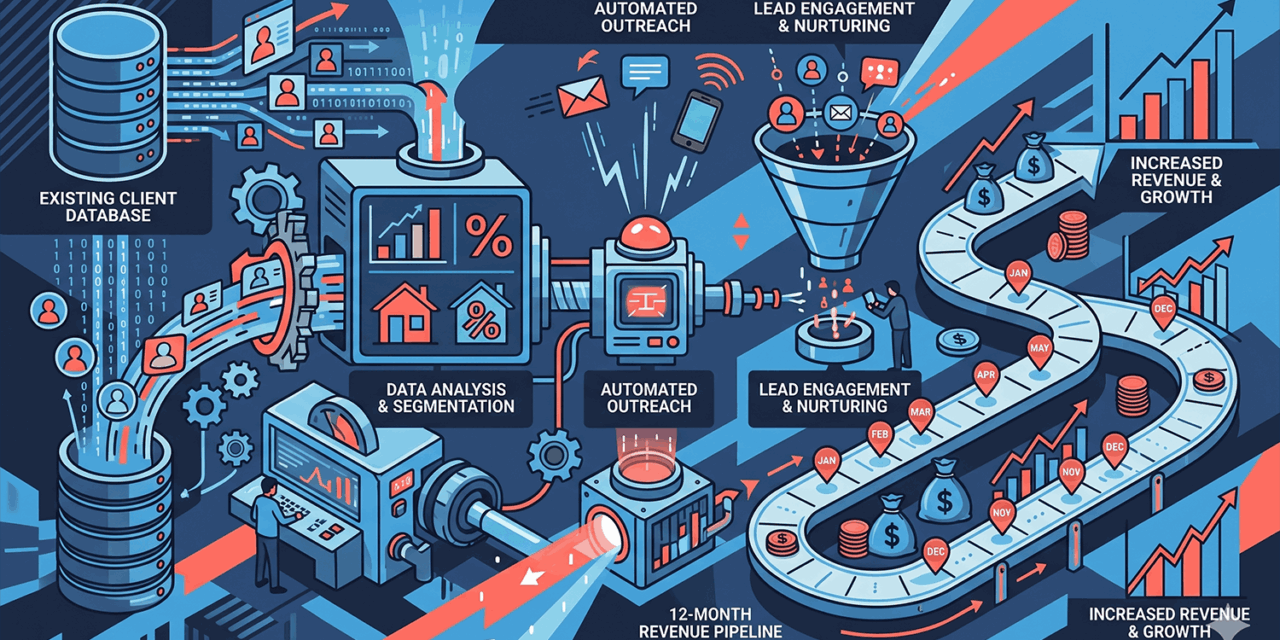

The Refinancing Outreach Machine

Refinancing activity up 15% YoY. Your database is a pipeline — here’s how to activate it.

4 Database Segments to Target

Fixed rate expired or expiring in 90 days. Currently on revert rate — highest financial urgency for refinancing conversation.

Settled 24+ months ago, no recent contact. Almost certainly not on best available product. Ripe for review.

Balances over $600K. Even 50 bps saving = $3,000+/year. The financial case is compelling enough to drive action.

Income increases, family changes, business growth — may now access better products or higher borrowing capacity.

The 4-Touch Follow-Up Sequence

Personalised email/SMS with specific repayment saving estimate.

Follow-up adding value — market commentary, rate move update.

Direct phone call. Leave genuine voicemail if no answer.

Final season touch. Park for 90-day re-cycle if no response after 4 contacts.

Automate vs. Personalise

- Fixed-rate expiry reminders (60/30/7 days)

- Settlement date milestone reviews

- Birthday and anniversary touchpoints

- Post-settlement satisfaction surveys

- Specific rate and product discussions

- Hardship or distress conversations

- Referral requests

- Any BID-sensitive recommendation conversations

Build your refinancing machine. Read the full guide.

May 2026

11 min read

The Refinancing Outreach Machine: Building a 12-Month Revenue Pipeline From Your Existing Database

Refinancing activity is up 15% year-on-year. Your existing client database contains more active pipeline value than you realise. Here is the system to unlock it.

Key Takeaways

- Segment your database into four priority tiers: fixed-rate expirees, long-settled clients, high-balance clients, and life-stage change clients.

- A structured 4-touch outreach sequence over 45 days converts dormant contacts into active pipeline.

- Personalised savings estimates — not generic emails — are the primary driver of outreach response rates.

- Automate mechanical triggers (fixed expiry reminders, milestone check-ins); keep rate and product conversations personal.

- The compound effect of systematic outreach builds referrals and reviews — not just refinanced loans.

The most underutilised asset in most brokerage businesses is sitting in a CRM that sends birthday messages and nothing else. In a market where refinancing activity has grown 15% year-on-year, the brokers building structured, systematic outreach programs are generating significant revenue from clients they already have.

Why the Refinancing Window Is Different Right Now

Three compounding dynamics make 2026 an unusually strong environment for database refinancing. First, rate divergence: clients settled in 2022–2024 may be on rates 80–120 basis points above the best available product — $4,000–$8,000 per year in unnecessary interest on a median loan. Second, non-bank lenders have dramatically improved their competitive positioning post-APRA DTI cap, making them genuinely competitive for profiles that would previously have defaulted to a major bank. Third, many fixed-rate loans written in 2023–2024 have already expired or will expire in the next 12 months, with borrowers sitting on revert rates and primed for a refinancing conversation.

Mapping Your Database: 4 Refinancing Segments

Segment 1 — Fixed-Rate Expirees (Highest Priority): Clients whose fixed rate has expired or expires within 90 days. Outreach should begin 60–90 days before the revert date. These clients are on premium pricing and the financial urgency is highest.

Segment 2 — Long-Settled Clients Without Review: Settled 24+ months ago, no recent contact. Filter for clients with no CRM activity in 12 months and settlement date older than 24 months. Almost certainly not on best available product.

Segment 3 — High Balance Clients: Balances above $600K where even a 50 basis point saving delivers $3,000+ per year. The financial case is compelling enough that outreach essentially sells itself when the saving is personalised.

Segment 4 — Life-Stage Change Clients: Income increases, family changes, business growth since settlement. These clients may access better products or higher borrowing capacity they are not aware of.

The 4-Touch Follow-Up Sequence

Day 0 — Personalised email or SMS with a specific estimated saving. Day 7 — Follow-up adding value: a rate movement update or relevant market commentary. Day 21 — Direct phone call attempt with genuine voicemail. Day 45 — Final season touch; park for 90-day re-cycle if no response. Do not chase beyond four touches — it damages the relationship.

Acknowledge the context. Present a concrete personalised saving. Make it easy to engage. Remove the obligation. This four-part structure consistently outperforms generic rate-comparison emails.

Measuring What Matters

Track monthly: outreach volume, response rate, appointment conversion rate, settlement conversion rate, average commission per settled refinance, and database coverage percentage. These metrics improve significantly in the first six months as you refine messaging and segmentation. Most brokers find their database has substantially more active pipeline value than they realised — it was simply dormant for lack of a consistent process.

The Compound Effect

A well-run database refinancing program generates referrals and reviews from clients who experienced proactive service when they needed it most. In a market where most borrowers believe their broker disappears after settlement, being the broker who actually stays in touch is a powerful competitive differentiator that compounds over every rate cycle.

More broker growth strategies at The Broker Times →

Database Segment Identifier

Answer 3 questions about a client to identify which refinancing segment they belong to and the ideal outreach approach.

When did this client last settle with you?

Read the full refinancing database guide →

Disclaimer: This article is for general information and professional development purposes only. It does not constitute legal, compliance, or financial advice. Brokers should consult their aggregator's compliance team and, where required, seek independent legal advice regarding their obligations under the National Consumer Credit Protection Act 2009 and ASIC's responsible lending guidelines.

{kind=link}