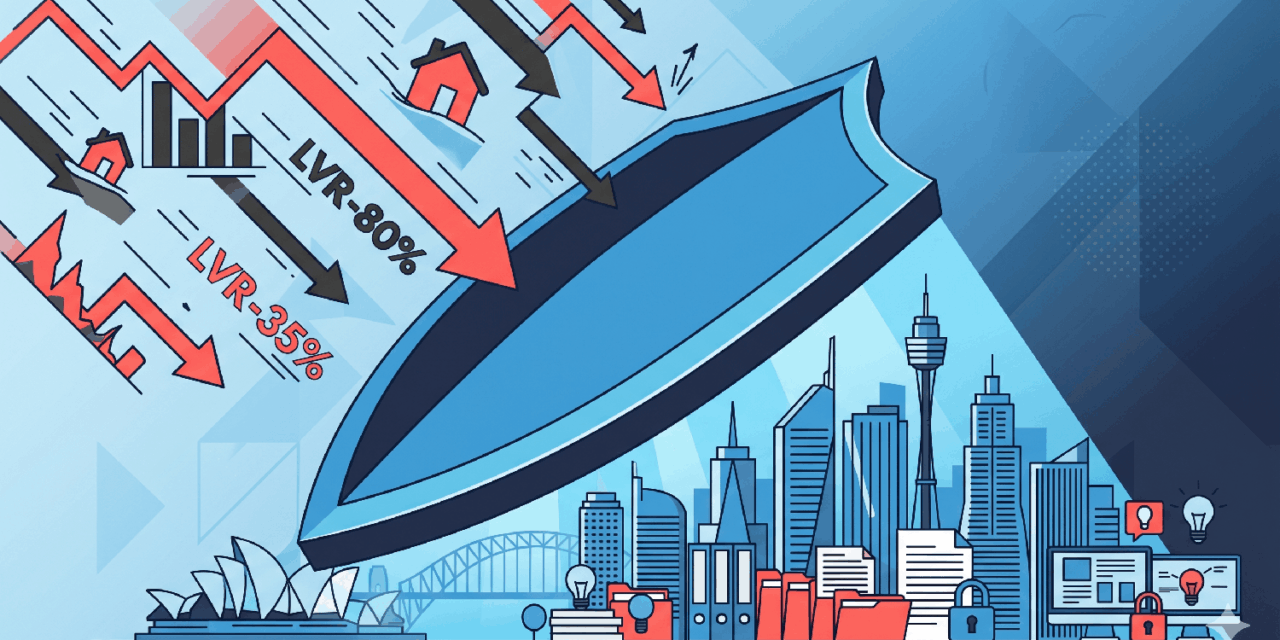

Valuation Risk in a Falling Market

Sydney and Melbourne recorded their first synchronised monthly price fall in 3 years in April 2026.

LVR Risk Zones in a Falling Market

LOW RISK

Strong equity buffer absorbs market correction. Full range of refinancing options available. Proactive outreach opportunity.

MONITOR

Still within standard range but monitor for further value erosion. AVM check before initiating refinancing conversations.

ELEVATED RISK

LMI threshold sensitive to further falls. Limited refinancing lender set. Non-bank lenders with higher LVR appetite are key. Manage client expectations proactively.

HIGH RISK

Very limited refinancing options. May require equity injection, guarantor, or deferred refinancing decision. Honest proactive conversation required under BID.

3 Valuation Methods: What Brokers Should Know

Pre-Lodgement Valuation Checklist

Run CoreLogic AVM estimate before initiating refinancing conversation

Pull comparable sales from past 90 days — not 12 months — for current market accuracy

Ask BDM about valuation panel performance in the specific postcode

Consider upfront valuation for borderline LVR files before full application investment

Set realistic client expectations on valuation range before lodging — removes shock if result is lower

Protect your client files in a falling market. Read the full guide.

May 2026

11 min read

Shrinking LVRs, Stalled Valuations: How to Protect Client Files When Sydney and Melbourne Property Values Fall

April 2026 delivered the first synchronised monthly price fall across both capitals in three years. Here’s how brokers can manage valuation risk and protect approvals in a softening market.

Key Takeaways

- Clients at 80–90% LVR from 2024 settlements may now sit above the LMI threshold if values have fallen.

- AVMs weight recent comparable sales heavily — they can be the most aggressive in a falling market. Full valuations are worth requesting on borderline files.

- A valuation that comes in short is not necessarily final — comparable sales review, BDM escalation, and alternative lenders are all worth pursuing.

- Pre-lodgement valuation intelligence (AVM check, recent comps, BDM conversation) is standard practice in a falling market.

- Manage client expectations on valuation range before lodging — it positions you as the informed advisor managing the process.

April 2026 delivered the first synchronised monthly price fall across Sydney and Melbourne in over three years. For brokers managing refinancing applications, construction loan transitions, and equity release files, the implications are real and immediate.

How a Falling Market Creates File Risk

The most direct risk is the LVR flip: a borrower who settled at 80% LVR and has been making repayments may find their LVR is higher today than at settlement if values have fallen materially. Clients at 85–90% LVR who have seen a further value decline may now be above 95% — dramatically narrowing their refinancing options. Knowing which clients are in this zone before initiating a refinancing conversation is critical.

The 3 Valuation Methods: What Brokers Need to Know

AVMs are fast and cheap but weight recent comparable sales heavily — making them the most aggressive method in a falling market. Desktop valuations are more considered but still subject to comparable sales. Full independent valuations account for specific property features that distinguish a property from comparables, often producing a more favourable result. For borderline LVR files, requesting a full valuation is worth the additional time and cost.

Request a comparable sales review, provide additional comps the valuer may have missed, escalate through your BDM, or approach a different lender whose panel may use different firms. A short valuation is not necessarily final.

Pre-Lodgement Valuation Intelligence

Build a pre-lodgement valuation check into your refinancing workflow: run a CoreLogic AVM, pull 90-day comparable sales (not 12-month), ask your BDM about postcode-specific valuation panel performance, and consider upfront valuations for borderline LVR files. Setting realistic client expectations on valuation range before lodging removes the shock element if results come in lower — and positions you as the professional managing the process.

The Opportunity Inside the Risk

Clients with strong equity positions — particularly those who purchased before 2020 and have not drawn down significantly — have very healthy LVRs even in a correcting market. For these clients, a falling market creates an opportunity to restructure debt, access equity, or reposition borrowing before values soften further. The skill is in knowing which clients face each dynamic and managing them accordingly.

More loan strategy insights at The Broker Times →

LVR Risk Checker

Estimate a client’s current LVR and valuation risk position in a falling Sydney or Melbourne market.

Enter client figures above to calculate LVR risk

Read the full valuation risk guide at The Broker Times →

Disclaimer: This article is for general information and professional development purposes only. It does not constitute legal, compliance, or financial advice. Brokers should consult their aggregator’s compliance team and, where required, seek independent legal advice regarding their obligations under the National Consumer Credit Protection Act 2009 and ASIC’s responsible lending guidelines.

{kind=link}