The Gist — 10-Second Read

- The budget’s negative gearing carve-out keeps the tax benefit for new builds, steering investor demand there.

- Loan Market’s investor new-vs-established ratio moved from 1:22 to 1:13 in a year — the tilt is already showing up.

- Off-the-plan lending is a different animal: progress payments, valuation at completion, and finance-approval expiry.

- The First Home Guarantee (5% deposit, no LMI, no place cap) makes new builds viable for FHBs too — expect competition for stock.

- Every off-the-plan recommendation needs a documented BID rationale covering completion and valuation risk.

The May budget didn’t just cool investor demand — it redirected the demand that survived. By keeping negative gearing for new builds while winding it back on established property, the government put a thumb on the scale for newly built stock, and the early data shows capital already moving that way. For brokers, that’s an opportunity with a catch: new-build and off-the-plan lending rewards a very different skill set to the established-purchase refi-and-buy work most books are built on. This is the playbook.

In this guide

Why Demand Is Tilting to New Builds

From the 12 May budget, negative gearing on established residential property is being wound back from 1 July 2027, while eligible new builds keep the ability to deduct losses against other income. Rational investor capital follows the exemption — and it’s already visible. As The Adviser reported, Loan Market’s ratio of investor loan applications for new versus established property moved from 1:22 in June 2025 to 1:13 in June 2026. Layer in the First Home Guarantee’s pull on FHBs toward new stock, and both cohorts are converging on the same segment.

Progress Payments and How the Money Flows

Off-the-plan and construction lending doesn’t settle in a single drawdown. Funds are released in progress payments aligned to build stages, and the client pays interest only on the amount drawn at each stage. Product is evolving fast here — CommBank, for example, extended progressive-drawdown funding to modular homes during the off-site factory build, funding up to 80% of the contract price before the home lands on site for accredited manufacturers.

Broker takeaway

Know which panel lenders handle progress payments cleanly, how they treat the land-plus-construction split, and how interest is serviced during the build. A client expecting a normal settlement can be blindsided by staged drawdowns and rising interest as the build progresses — that’s a conversation to have up front.

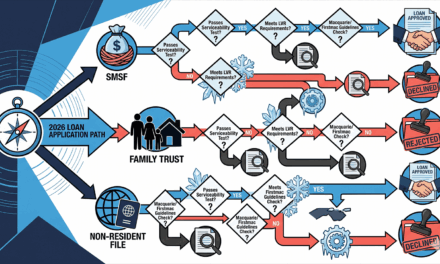

Off-the-plan · Risk watch-list

Four things to check before you recommend

General information only. Confirm current lender policy directly.

The Valuation-at-Completion Trap

This is the risk that catches clients — and thin files — most often. With off-the-plan, the lender values the property at settlement, not at the contract price. Where more than a year has passed between exchange and completion, some lenders assess against market value rather than the agreed price when setting the LVR, LMI premium and final loan amount. If the valuation lands below the purchase price, the LVR jumps, the deposit suddenly looks smaller, and the client can face additional cash or higher LMI at the worst possible moment.

How to protect the client

Set the expectation at the start: a rising market makes this a non-issue; a flat or falling one doesn’t. Build a cash buffer into the plan, and know which lenders are most conservative on completion valuations so you can steer the file accordingly.

Finance-Approval Expiry and Sunset Clauses

Approvals aren’t forever, and builds routinely run past a year. That means a formal approval today may need re-assessment before completion — on the client’s income, the lender’s policy, and the valuation as it stands at settlement. Add the developer’s sunset clause to the picture, and there are two clocks running on every off-the-plan file. Map both at the outset and diarise the re-assessment well before the build completes.

The First Home Guarantee Angle

New builds aren’t just an investor story. The First Home Guarantee lets eligible first home buyers purchase or build with a 5% deposit while the government guarantees up to 15% of the price — dropping the lender’s effective risk to 80% LVR and removing LMI. With place caps and income caps now gone, the addressable FHB pool for new builds is materially larger than it was a year ago.

The competition angle

Here’s the tension to flag with clients: investors chasing the negative gearing carve-out and FHBs using the guarantee will increasingly compete for the same new-build stock. Brokers with developer and project-marketing relationships — and product to point clients at — will win that scramble.

Off-the-Plan and Best Interest Duty

Steering a client toward a new build carries a heavier evidence burden than an established purchase, precisely because of completion and valuation risk. Your file should show you discussed the valuation-at-completion scenario, the finance-expiry and sunset-clause risks, and why the new-build path suits this client’s objectives. A thin note ages badly if a valuation lands short at settlement — document the trade-offs while they’re front of mind, not after a problem appears.

Building a New-Build Channel

- Map your panel for progress-payment strength and completion-valuation policy.

- Build developer and project-marketing relationships so you have compliant, quality stock to point clients at.

- Create a client-ready off-the-plan explainer covering staged drawdowns, valuation risk and timelines.

- Diarise re-assessment triggers for every off-the-plan file well ahead of completion.

The Bottom Line

The budget turned new builds from a niche into the segment the market is tilting toward — and the brokers who profit from it will be the ones fluent in how off-the-plan money actually flows. Master progress payments, get ahead of the valuation-at-completion trap, track the two clocks on every file, and document your BID rationale. Do that, and the new-build pivot is a growth lane while other brokers are still treating it like an established purchase with a longer settlement.

Disclaimer: General information and professional-development content only; not legal, tax or financial advice. Lender policies on progress payments, complet

{kind=link}