Too Busy to Read? We’ve Got You.

Get this blog post’s insights delivered in a quick audio format — all in under 10 minutes.

This audio version covers: The Trust Lending Freeze Spreads: A 2026 Decision Tree for SMSF, Family Trust and Non-Resident Files After Macquarie and Firstmac

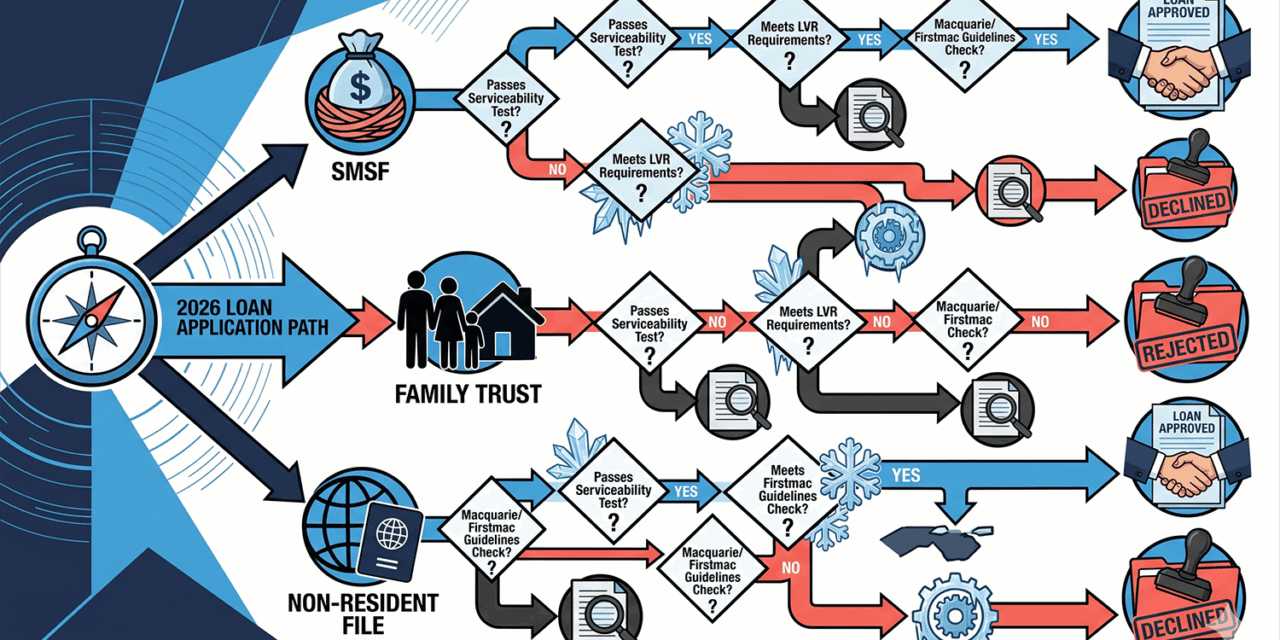

The 4-Band Trust Panel

After Macquarie and Firstmac — how the trust-lending panel actually divides today, and how to route the file.

Macquarie’s pause on new home loans to trusts and companies in mid-May 2026, followed by Firstmac’s tightening of trust-related serviceability the week after, has done something that did not happen in any single trust-policy adjustment over the past five years: it has made trust files materially harder to place, across the panel, all at once. Specialist lenders are still open. The majors are pulling back. The non-banks are dividing into “open with conditions” and “effectively closed” camps, and the lines are moving weekly.

For brokers handling SMSF residential, discretionary family-trust property purchases, and non-resident-borrower trust structures, the operational reality has changed faster than most aggregator policy update emails have caught up. This piece is the decision tree for the 2026 trust-lending file: what to ask, who to call, when to pivot to an alternative structure, and when to hold the file until the policy environment settles.

Why the Freeze Spread

Three factors converged. Aggressive social-media-driven structuring strategies pushed trust-based property acquisition volumes well above historical norms in 2024–25, surfacing concentration risk. Compliance complexity on guarantor structures, beneficiary documentation, and beneficial-ownership disclosure has increased — particularly under AUSTRAC’s 1 July 2026 referral-partner reforms. And the post-budget tax change has added a layer of uncertainty about how the negative gearing and CGT regime will treat trust-held property going forward.

Macquarie’s pause was framed as compliance-driven. Firstmac’s policy update was framed as risk-driven. The aggregate effect is the same: trust files require more lender-specific knowledge in 2026 than they did 12 months ago, and the broker who treats a trust file as a standard residential application will burn weeks placing what should be a four-week settlement.

Where the Panel Sits Right Now

The trust-lending panel as of June 2026 divides into four broad bands.

Band A — open with broad appetite: A small group of non-bank lenders and specialist lenders continues to write trust-structured residential and SMSF lending with relatively standard process. ORDE Financial, La Trobe, and several second-tier specialists sit in this band. Pricing is wider than major-bank pricing but turnaround is reliable.

Band B — open with conditions: Several non-banks and a couple of mutuals remain open but have introduced additional documentation requirements, lower LVR ceilings, or restrictions on beneficiary composition. Brighten, ME Bank (corporate trustee files), and Pepper sit broadly in this band, with policies moving weekly.

Band C — effectively closed for new business: Macquarie’s pause is the most visible example. Firstmac has not paused outright but has tightened to the point where new trust applications are routinely declined for guarantor or serviceability reasons. Several major bank arms have quietly stopped pursuing trust-channel volume.

Band D — bespoke and case-by-case: The major bank private-bank channels remain open for high-net-worth trust files, but on a relationship-driven, case-by-case basis. Useful for the right client; not a volume play.

The Trust-Lending Decision Tree

Decision 1: Is the trust structure essential, or convenient?

This is the first question, and it is the one most brokers skip. For some clients, the trust structure is essential — usually for asset protection, tax structuring approved by their accountant, or SMSF-specific legal requirements. For others, the trust was suggested in a property seminar or by a social media commentator and the client cannot articulate why it matters for them specifically.

For essential-trust clients, proceed with structure intact and route to the appropriate lender band. For convenient-trust clients, the broker conversation should explicitly raise the option of personal-name purchase. In a tighter trust-lending environment, the personal-name route is faster, cheaper, and often delivers the same long-term outcome with less complexity. Document the client’s decision either way for the BID file note.

Decision 2: SMSF, discretionary trust, or hybrid structure?

SMSF residential lending sits in its own policy track at most lenders. Limited recourse borrowing arrangements have specific documentation requirements (corporate trustee, custodian, single asset rule) and a narrower lender appetite. Specialist SMSF lenders — Liberty, Granite Home Loans, La Trobe — remain reliably open with experienced processing teams.

Discretionary family trusts get hit hardest by the current tightening. Beneficiary documentation, vesting dates, settlor identity, and trust deed clauses are all under heavier scrutiny. The lender band that will accept the file depends heavily on the trust deed quality.

Hybrid and unit trust structures are the hardest to place in 2026. Most major-bank channels have closed; only a small group of non-banks and specialist lenders will consider them, and only with strong serviceability and documentation.

Decision 3: What is the guarantor structure?

Guarantor exposure is the single biggest lender-by-lender variable in trust files this year. Firstmac’s recent tightening explicitly named guarantor structures as the driver. Most lenders now require all guarantors to be included in the serviceability assessment for the full loan amount, eliminating the structuring leverage trust files used to provide.

If the application has multiple beneficiaries, multiple corporate-trustee directors, and multiple personal guarantors, expect a longer assessment and a narrower lender list. If the guarantor structure is clean — corporate trustee, one personal guarantor, full disclosure of beneficiary income where relevant — the file is materially more placeable.

Decision 4: What is the borrowing purpose?

Owner-occupier trust purchases are now a narrow lender set. Investor trust purchases sit in a wider but tightening set. SMSF residential is its own category. Construction loans through trust structures are the most difficult to place under current settings — most lenders have either paused or imposed enough conditions that the file is impractical.

Decision 5: What is the timeframe?

If the client has a 30-day finance clause, this is a high-risk file in the current environment. Trust-file turnaround across the active panel has lengthened by 5–15 business days in the past six weeks. If your client has signed a contract with a tight finance clause, the conversation needs to include the realistic possibility of needing an extension.

If the client has flexibility on timing, the file is much more manageable, and the broker can hold for a lender response without commercial pressure forcing a sub-optimal lender choice.

Practical Operational Steps

Audit your active trust files this week. Any file that is currently with a Band C lender (Macquarie, Firstmac-restricted, or paused major) needs a parallel application lodged with a Band A or B lender now, not after the decline. Lender turnaround for trust-aware non-banks ranges from 7 to 15 business days at present; do not assume a re-submission will hit the same SLA you were planning around.

Build a one-page trust file briefing template for your processing team. Trust deed (with vesting date and beneficiary class), corporate trustee constitution, full guarantor schedule, beneficiary income where relevant, ATO trust tax records for the last two years. This is the documentation that the current trust-aware lenders are asking for. Files arriving without this set get sent back for additional information and the SLA clock resets.

Set up a quarterly review call with your aggregator’s specialist lending desk. The trust-lending policy environment is moving too quickly for once-a-year panel discussions to keep pace. Most aggregator specialist desks have direct lender-relationship visibility that brokers cannot replicate alone.

Identify two trusted property-law solicitors and one accountant with deep trust-structure experience. Many trust files are slowed not by lender policy but by trust deed quality. The broker who can route a client to a solicitor for a deed review before submission saves weeks.

Risks and Blind Spots

The biggest BID risk in the current environment is the broker who proceeds with a trust file on the assumption that “the lender we used last year will be fine this year.” Trust-lending policy is the most dynamic policy track in residential lending right now. Every trust file should be confirmed against current published policy before submission.

A second risk is recommending a structure change mid-process. If a client originally engaged with you on a trust purchase and you advise pivoting to personal-name acquisition, the file note needs to capture the rationale, the alternative structures considered, the lender options available under each, and the client’s informed decision. ASIC’s BID review has flagged structural recommendations as an area of specific interest, particularly where the broker is positioned to influence the client’s structural choice.

A third risk is the AUSTRAC referral-partner overlay. From 1 July 2026, certain trust-related referrals fall under expanded AML/CTF obligations. Your AUSTRAC compliance must be current before you accept or refer trust-structured business in the second half of 2026.

Opportunities

Trust lending in the current environment is a specialist channel. Brokers who develop genuine expertise — current panel knowledge, deep documentation discipline, strong solicitor and accountant referral networks — sit in a small minority of the broker channel and command higher trust and higher conversion rates from a smaller pipeline.

Referral-partner relationships are the highest-leverage marketing play available to trust-experienced brokers. Property accountants, family lawyers, and SMSF specialists are fielding trust-financing questions weekly and have very few experienced brokers to refer to. A single 30-minute introductory meeting with a property-accountant practice often produces three to five trust files over the following six months.

The third opportunity is positioning for the post-tightening reset. The current policy environment will not last forever. Lenders that are currently closed or restricted will reopen, sometimes with a sharper appetite for the segment they paused on. Brokers with current trust-channel experience and a database of waiting clients will be best positioned to capture the volume when policy loosens.

Conclusion

Trust lending in mid-2026 is not closed — but it is a different business than it was 18 months ago. The decision tree is longer, the lender list is shorter, the documentation discipline is higher, and the BID file expectations are sharper. The brokers who build a structured, current, defensible process for these files will keep writing them. The brokers who treat trust files as standard residential applications will spend the second half of 2026 explaining to clients why their finance clause has been extended for the third time. Use the decision tree. Audit the panel. Build the referral network. Document the BID position. And keep the trust file moving while everyone else waits for the policy environment to settle.

Broker Action Checklist

- Audit every active trust file against current panel policy this week

- Lodge parallel applications for any file currently with a paused or restricted lender

- Build the trust-file briefing template (deed, trustee, guarantors, income, ATO records)

- Schedule a specialist-lending review with your aggregator BDM this quarter

- Identify two property-law solicitors and one trust-specialist accountant for referral

- Refresh AUSTRAC compliance ahead of 1 July 2026 reforms

- Build the BID file note template that captures structural recommendation rationale

Disclaimer: This article is for general information and professional development purposes only. It does not constitute legal, compliance, or financial advice. Brokers should consult their aggregator’s compliance team and, where required, seek independent legal advice regarding their obligations under the National Consumer Credit Protection Act 2009 and ASIC’s responsible lending guidelines.

{kind=link}