Too Busy to Read? We’ve Got You.

Get this blog post’s insights delivered in a quick audio format — all in under 10 minutes.

This audio version covers: The Privacy Exemption Cliff and Data Liability Strategy A Research Report for the Australian Mortgage Broking Industry

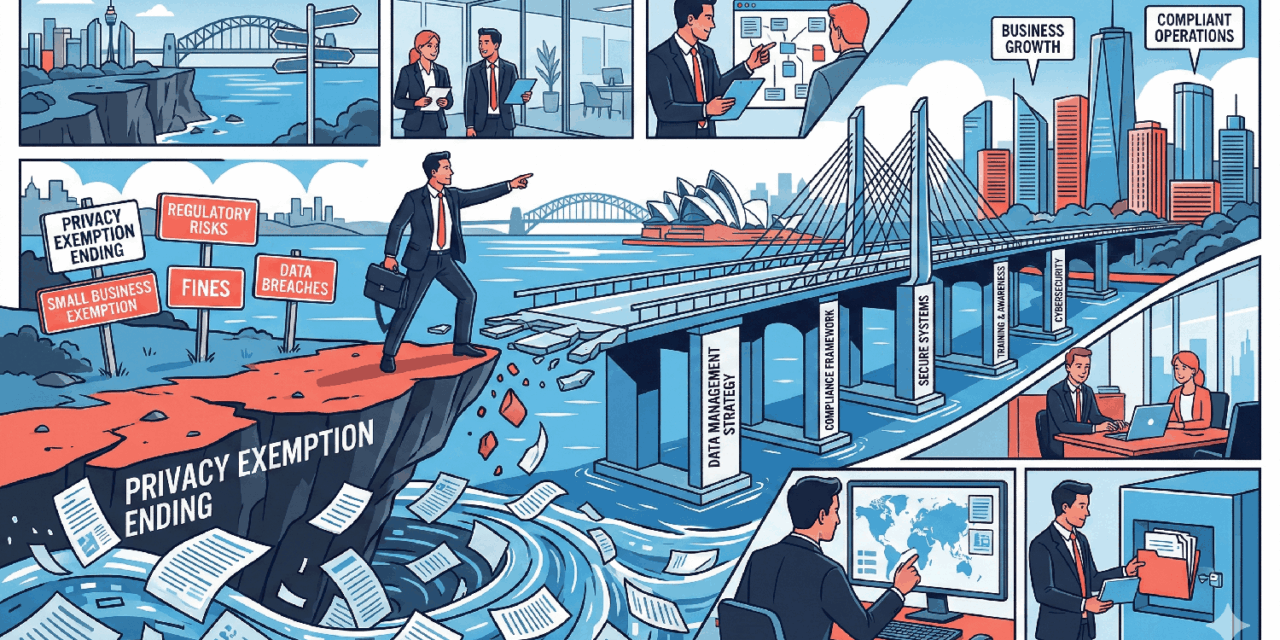

The Privacy Exemption Cliff and Data Liability Strategy

The era of the “free pass” is over. Historically, 95% of Australian mortgage brokerages have operated under the small business exemption, shielded from the full weight of federal privacy law. As we move toward 2026, the legislative “buffer” is slated for abolition, compelling firms to navigate a new landscape of “fair and reasonable” data handling and multi-million dollar penalties.[2, 3, 4]

Inside This Briefing:

Step 1: Strategic Realignment

For decades, entities with an annual turnover under $3 million have been exempt from the *Privacy Act 1988*.[3, 5] However, the nature of data held by brokers—ranging from Tax File Numbers to granular expenditure patterns—is now viewed as high-risk, regardless of the firm’s revenue.[3, 6]

Central to these changes is the introduction of a positive obligation: data collection must be “fair and reasonable” in the circumstances. This moves the industry away from simple “bundled consent” toward an objective standard of conduct where even explicit consent will not shield a broker if the data handling is deemed disproportionate.[7, 9, 10]

Step 2: The Data Liability Trap

Mortgage brokers are uniquely vulnerable to a “Data Liability Trap.” Competing regulatory obligations often force brokers to accumulate highly sensitive “honeypot” data for extended periods.[11, 6]

The AML/CTF Conflict

Proposed Tranche 2 AML reforms will require brokers to verify beneficial owners of complex structures, retaining sensitive identity documents (passports, trust deeds) for seven years.[11, 6] This accumulation makes brokerages prime targets for cybercriminals. If a breach occurs, brokers face dual-pronged liability: scrutiny from the OAIC and potential negligence claims from clients.[11]

Step 3: The Penalty Landscape

The enforcement landscape is being redesigned with “sharper powers” for the regulator and a new cause of action for individuals.[12, 4]

| Penalty Tier | Nature of Breach | Maximum Penalty (Body Corporate) |

|---|---|---|

| Top Tier | Serious interference with privacy [7, 13] | Greater of $50M, 3x benefit, or 30% turnover [14, 5] |

| Middle Tier | Interference falling short of “serious” [7] | Up to $3.3 Million [7, 13] |

| Bottom Tier | Procedural failings (e.g., missing policy) [7, 13] | Infringement notices up to $330,000 [7, 13] |

| Civil Tort | Serious invasion of privacy [7, 15] | $478,550 Capped Damages [16, 17] |

Step 4: The Training Mandate

Recent amendments to APP 11 clarify that “reasonable steps” to protect data include organisational measures, not just technical ones.[18, 19]

Regulators will now investigate whether a firm maintained a verified training register and documented internal policies for data handling.[12, 20, 21] For the broker, this means a staff member falling for a phishing attack could trigger a firm-wide breach investigation.[22]

Step 5: Cyber-Resilience Blueprint

Cyber-resilience is the capacity to withstand, recover from, and adapt to shocks.[8, 19] In 2026, it is “integral to operational performance”.[19]

Implementation Roadmap

- Data Discovery: Audit what you hold. If you don’t need it, delete it. If you must keep it (AML), encrypt it.[11, 12, 23]

- Privacy-by-Design: Conduct Privacy Impact Assessments (PIAs) *before* implementing new CRMs or AI tools.[7, 10, 24]

- Incident Readiness: Test a data breach response plan to ensure you can notify the OAIC within 72 hours.[25, 12, 26]

- Consumer Trust: 94% of consumers prioritize data security in AI-powered finance. Transparency is now a primary marketing differentiator.[15, 27, 28, 29]

{kind=link}