The Gist — 10-Second Read

- The ban on new residential SMSF LRBAs commences 10 August 2026 (Royal Assent 26 June).

- Contracts exchanged before commencement are protected — even if settlement lands after.

- Existing LRBAs are grandfathered, refinancing is still allowed, and commercial property is unaffected.

- The realistic runway for a new fund + purchase is tight — establishment, rollover, bare trust and finance all have to clear.

- Do not let the deadline push an unsuitable strategy through. BID and SIS-compliance don’t relax because a clock is ticking.

The uncertainty is over, and the clock is now the story. With the Treasury Laws Amendment (Tax Reform No. 1) Bill 2026 receiving Royal Assent on 26 June, the ban on using a new Limited Recourse Borrowing Arrangement (LRBA) to buy residential property inside an SMSF is locked to commence 10 August 2026. For any client with an SMSF residential purchase in mind, the question has shifted from “will this change?” to “can we exchange in time?” This is your final-window execution playbook — and the compliance guardrails that still apply while everyone’s in a hurry.

In this guide

- What actually changes on 10 August

- What’s unaffected: grandfathering, refinancing, commercial

- The contract window: what “in time” really means

- The 30-day execution timeline

- Which clients to call this week

- The BID trap in a deadline rush

- Life after the ban: where the SMSF conversation goes

- The bottom line

What Actually Changes on 10 August

From 10 August 2026, an SMSF will no longer be able to establish a new LRBA to acquire residential property. The Bill moved through both houses in under 48 hours after the government secured Greens support, so the runway between assent and commencement is unusually short. As reported by The Adviser, brokers writing SMSF business are among the most time-pressured parties in the chain, alongside trustees, solicitors and SMSF administrators.

What’s Unaffected: Grandfathering, Refinancing, Commercial

The ban is narrower than the headlines suggest. It does not touch:

- Existing residential LRBAs established before 10 August 2026 — fully grandfathered and able to run their course.

- Refinancing of an existing LRBA — explicitly permitted under the legislation.

- Residential property owned outright by an SMSF (no borrowing).

- Commercial property and business real property LRBAs — unaffected, which keeps the door open for business-owner clients buying their own premises through super.

Why it matters

Two of these are live opportunities, not just carve-outs. The refinancing carve-out means your existing SMSF-loan clients still have a market to be re-priced into. And the commercial/business-real-property exemption is where a lot of SMSF lending conversation will migrate after August — worth flagging now with self-employed clients.

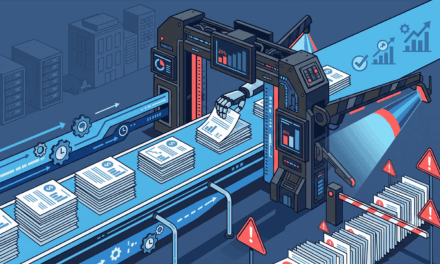

Countdown · Residential LRBA ban

The chain that must clear before 10 August 2026

Exchange before commencement and you’re protected — even if settlement is after 10 August.

General information only. Source: Treasury Laws Amendment (Tax Reform No. 1) Bill 2026; The Adviser; iCare Super.

The Contract Window: What “In Time” Really Means

The protection hinges on the acquisition arrangement — in practice, exchanging contracts — being entered into before commencement. If contracts are exchanged before 10 August, the purchase is protected even where settlement occurs afterward. Miss the exchange and no amount of “we were nearly there” changes the outcome. That single hinge is what makes the next four weeks a genuine execution problem rather than a planning one.

The 30-Day Execution Timeline

For a brand-new fund, the critical path is unforgiving. Working backwards from a contract exchange in the first week of August:

- Now: confirm the client genuinely wants (and suits) an SMSF residential purchase; start fund establishment and rollovers immediately if so.

- Week 1–2: fund registered, bank account open, rollovers requested, bare trust drafted, lender selected and application in.

- Week 2–3: valuation and formal approval; solicitor and conveyancer aligned on the bare-trust structure.

- Before 10 Aug: contracts exchanged. Build in buffer — rollover timeframes and lender turnarounds are the usual choke points.

Reality check

Rollover timing and SMSF-loan turnarounds are outside your control and rarely fast. If a client is starting from zero today, be honest about whether the chain can realistically clear — a rushed, half-formed structure is worse than a missed deadline.

Which Clients to Call This Week

- Clients mid-conversation about SMSF property — they need a clear go/no-go today, not in a fortnight.

- Existing SMSF-loan clients — the refinancing carve-out means a re-price is still on the table.

- Self-employed clients eyeing their own premises — the commercial/business-real-property route is unaffected and worth introducing now.

The BID Trap in a Deadline Rush

A ticking clock is exactly the environment where Best Interest Duty files get thin. SMSF lending already sits under heightened scrutiny, and “the ban was about to start” is not a substitute for a documented suitability assessment. The urgency is real, but it doesn’t lower the bar — if anything, ASIC will look harder at SMSF files exchanged in the final weeks. Keep your record of the client’s objectives, the alternatives considered, and why an LRBA suits, current and complete.

Life After the Ban: Where the SMSF Conversation Goes

The residential door closing doesn’t end SMSF lending — it redirects it. Expect the conversation to concentrate around commercial and business real property, refinancing existing arrangements, and non-geared residential strategies (buying outright within super). Brokers who build fluency in those pathways now will still have an SMSF story to tell clients in September.

The Bottom Line

The 10 August commencement turns a policy debate into a scheduling problem. For clients who genuinely suit an SMSF residential purchase and can realistically exchange in time, the next four weeks are about disciplined execution and honest timelines. For everyone else, the smarter play is to pivot the conversation to the carve-outs that survive — commercial, business real property and refinancing — and to protect your files while the market rushes. Beat the deadline where it’s right; never let the deadline beat your compliance.

Disclaimer: General information and professional-development content only; not legal, tax or financial advice. SMSF and LRBA structures are complex and outcomes depend on individual circumstances. C

{kind=link}