The Gist — 10-Second Read

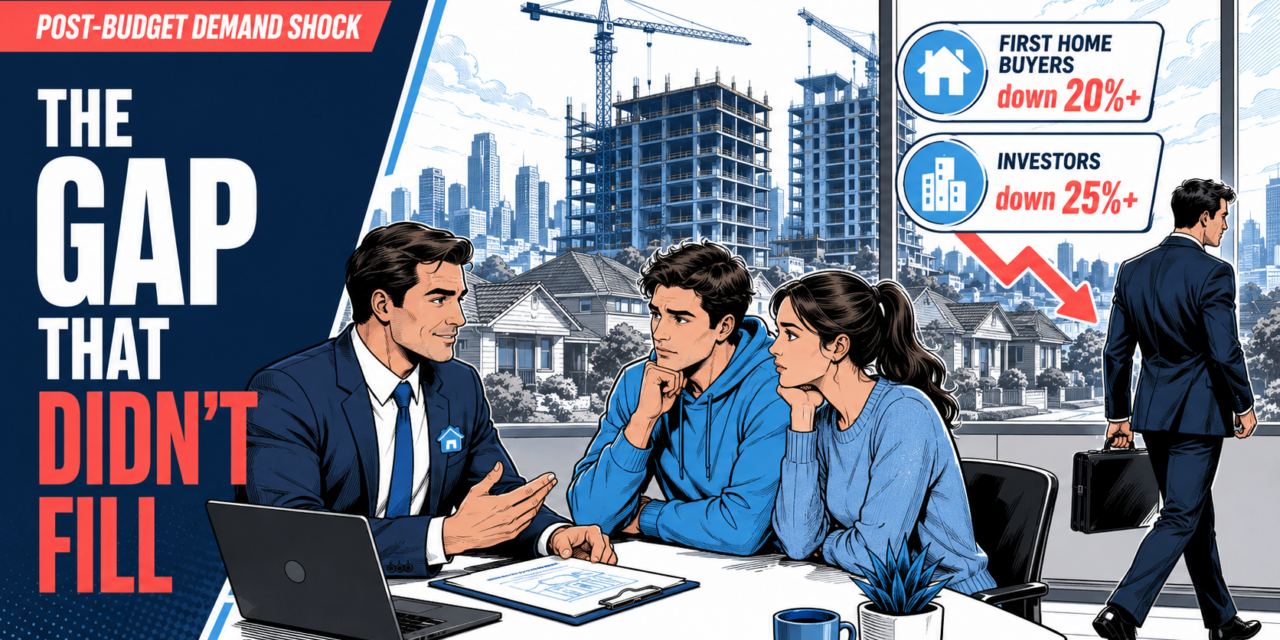

- Aussie Home Loans: FHB lodgements down 20%+ and investor lodgements down 25%+ since the 12 May budget.

- Loan Market: FHB applications fell 16% and investor applications 19% in June vs the four weeks pre-budget.

- The government’s bet — that FHBs would fill the space investors vacated — hasn’t happened. Both engines cooled at once.

- Remaining demand is tilting to new builds: Loan Market’s investor new-vs-established ratio moved from 1:22 to 1:13 in a year.

- Investor borrowing power is being cut now by servicing recalibration — a 2027 tax change biting in 2026.

The federal government’s May budget was meant to rebalance the market — push investors out of established housing and open space for first home buyers. Ten weeks on, the data tells a different story. Fresh figures from Aussie Home Loans and Loan Market Group show both cohorts have pulled back sharply since 12 May, with first home buyers retreating almost as fast as investors. The gap the budget was meant to open for FHBs hasn’t been filled — both demand engines cooled at once, and that’s now a pipeline problem sitting on your desk.

In this guide

The Numbers: Two Demand Engines Cooling at Once

Two of the country’s largest broker networks have now put numbers to what many brokers have felt in their diaries since May: the phones went quiet on both sides of the ledger. According to figures reported by The Adviser, the retreat has been broad and fast.

Lendi Group CEO Sebastian Watkins, whose group operates Aussie Home Loans, put it bluntly: “Since the announcement on May 12, first home buyer lodgements have declined more than 20 per cent.” Investors moved harder still — “Over the same period, investor lodgements declined more than 25 per cent, indicating a much sharper pullback,” he said. Loan Market executive chairman Sam White reported the same shape: FHB loan applications down 16% in June and investor applications down 19%, both against the four weeks before the budget.

The Broker Times · Data

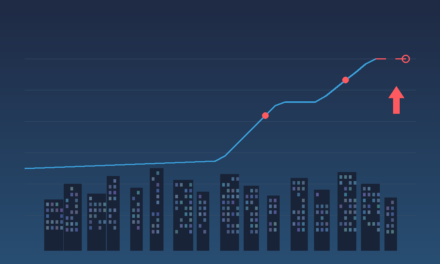

Lodgement decline since the 12 May budget

New-vs-established investor apps: 1:22 (Jun 2025) → 1:13 (Jun 2026) — demand is tilting to new builds.

Source: The Adviser (7 Jul 2026) · Aussie Home Loans · Loan Market Group.

Different networks, different metrics, same story: a double-digit contraction across both borrower types within weeks of the budget. This isn’t a soft patch in one segment — it’s a simultaneous cooling of the two engines that drive most residential broker pipelines.

The Gap That Didn’t Fill

The logic behind the budget’s housing package was straightforward: wind back negative gearing on established property, channel investors toward new supply, and let cooling investor competition give first home buyers room to step in. Treasury suggested the changes could help put around 75,000 homes within reach of FHBs.

Why it matters

That’s not what the early data shows. Watkins was direct: “The expectation was that first home buyers would step into the gap left by investors. That’s simply not what we’re seeing.” A market where investors pause and FHBs surge is a pipeline you can re-weight. A market where both pause is a volume problem no single cohort backfills — and it lands hardest on brokerages that assumed the FHB channel would absorb the slack.

Why Investors Bolted First: The Negative Gearing Cutover

Investors reacted fastest because the change aimed squarely at their maths. From the 12 May budget:

- Negative gearing on established residential property is removed from 1 July 2027 for properties bought after 7:30pm on 12 May 2026. Losses on established stock will only be deductible against rental income or a capital gain — not salary and wages.

- New builds are exempt — investors buying eligible new builds keep the ability to deduct losses against other income.

- Existing holdings are grandfathered — property held (or under contract) as at 7:30pm on 12 May 2026 can keep being negatively geared until sold.

- CGT is changing too — the 50% discount is being replaced with inflation-adjusted indexation, alongside a new minimum tax rate on certain gains.

The tax change itself doesn’t bite until 1 July 2027. But investors — and their lenders — have already priced it in. That’s the behavioural story behind the 25% lodgement drop.

The Servicing Timing Trap: A 2027 Change Cutting Borrowing Power in 2026

The trap

Here’s the point most likely to blow up a client conversation this month. Even though the negative gearing change is more than a year away, lenders have begun hard-wiring it into servicing calculators now. Several majors, led by CBA, have adjusted how negative gearing add-backs flow through assessments — quietly trimming investor borrowing capacity today for a rule that starts in 2027. White noted investor borrowing capacities had “taken a hit this month” as lenders reweight the settings.

A client who could borrow a certain amount in April may find their number has moved in July, for a rule that doesn’t commence until July 2027. If you can’t explain that gap clearly, the client hears “the goalposts moved” and disengages. Walk them through it calmly and you become the adviser who made sense of it.

Why First Home Buyers Didn’t Step Up: Uncertain, Stretched, Exhausted

If investors were spooked by policy, FHBs were worn down by everything else. White noted their applications had been softening before the budget — “rising house prices earlier in the year combined with decreased borrowing capacities due to the cash rate increases.” Watkins framed the mood from the front line: “When our brokers speak with customers, we’re hearing three things: they’re uncertain, they’re stretched, and they’re exhausted.”

Confidence, not eligibility, is the binding constraint. The addressable pool of FHBs hasn’t shrunk — arguably it’s improved, with First Home Guarantee income caps gone and prices softening in several markets. What’s missing is conviction. That’s a broker problem to solve, not a policy one to wait out.

The New-Build Tilt: Where the Remaining Demand Is Going

The demand that hasn’t evaporated is moving. Loan Market’s ratio of investor loan applications for new versus established properties moved from 1:22 in June 2025 to 1:13 in June 2026 — a pronounced structural tilt in a single year. The driver is the negative gearing carve-out: if losses on established property stop being deductible against other income but new builds keep that treatment, rational capital follows the exemption.

The broker skill gap

New-build and off-the-plan lending isn’t established-property lending with a different address. It carries progress payments, longer settlement runways, valuation risk at completion, developer due diligence, and finance approvals that can lapse before a build finishes. A book weighted to established resales needs to rebuild that muscle quickly.

What This Means for Your Pipeline

Strip out the policy noise and three things are true right now:

- You can’t assume FHB volume backfills investor volume. Model your next two quarters on both cohorts being softer, not one compensating for the other.

- The remaining demand rewards new-build capability. Fluency in progress payments, completion valuations and developer due diligence is shifting from “nice to have” to a differentiator.

- Servicing has moved ahead of the law, and clients don’t know it. The highest-value conversation you can have this month is explaining why an investor’s capacity changed before the 2027 rule commenced.

There’s a Best Interest Duty thread through all of this: recommending a new-build or off-the-plan pathway to a client who came in for an established purchase demands a documented suitability rationale — the completion-risk and valuation-gap trade-offs belong on file, not just in the pitch.

Your Next 30 Days: A Broker Action Plan

- Segment your pipeline by cohort and re-forecast. Flag every live investor file running on pre-budget servicing and re-run capacity on current calculators before you re-quote.

- Write the servicing-timing explainer once. A short, plain-English note on why capacity moved ahead of the 2027 change — reusable across every investor conversation.

- Stand up a new-build channel. Line up developer and project-marketing contacts; confirm which panel lenders are strongest on progress payments and completion-valuation policy.

- Re-engage stalled FHB leads with a clarity-first message. The pool is cautious, not gone — lead with what’s changed, what hasn’t, and why softer prices may work in their favour.

- Tighten file notes on any new-build recommendation to keep BID evidence current.

The Bottom Line

The May budget didn’t rotate the market from investors to first home buyers — it cooled both at once and pushed the demand that’s left toward new-build stock. Waiting for FHB volume to backfill the investor retreat is a losing strategy, because the data says that swap isn’t happening. The brokers who come out ahead will re-tool for new-build lending, get in front of the servicing-timing gap before clients feel blindsided, and lead a cautious FHB cohort with clarity. Watch the July–August lodgement data, further lender servicing changes, and the 10 August SMSF borrowing deadline landing another structuring pressure on investor conversations.

Disclaimer: General information and professional-development content only; not legal, tax or financial advice. Figures and quotes are drawn from reporting by

{kind=link}