Too Busy to Read? We’ve Got You.

Get this blog post’s insights delivered in a quick audio format — all in under 10 minutes.

This audio version covers: Monetising the ‘Borderline’ Database Building a 24-Month Pipeline of Previously Declined Applicants

Monetising the ‘Borderline’ Database: Building a 24-Month Pipeline of Previously Declined Applicants

In 2026, the Australian mortgage landscape is defined by a brutal paradox: property values are climbing at 6-7% annually, yet borrowing capacity is trapped under the ceiling of sustained high interest rates and unyielding APRA serviceability buffers.

For brokers, this means more “soft declines” at the inquiry stage. But a client who fails the assessment today isn’t a lost lead—they are deferred revenue. This article outlines the strategy for engineering a “rehabilitation” pipeline that turns 2026’s serviceability victims into 2028’s settled volumes.

In This Strategy Guide:

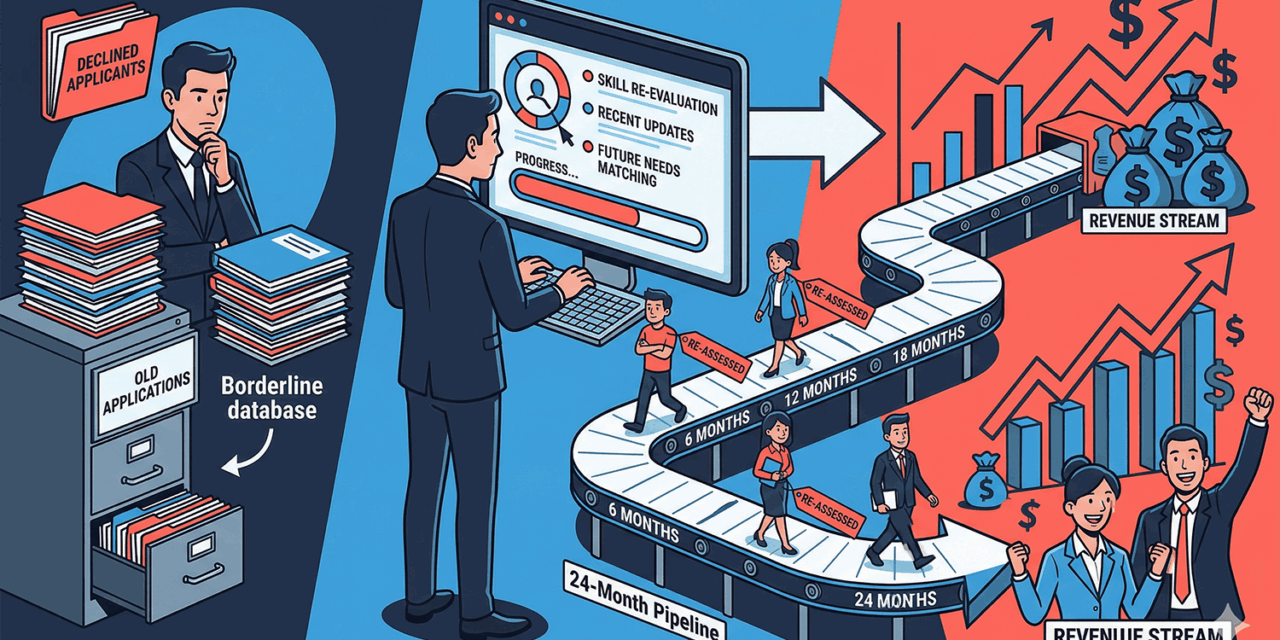

Step 1: The Triage – Segmenting Your Data

The first mistake most high-volume brokerages make is treating a serviceability failure as a binary “No.” To build enterprise value in 2026, you must segment your database by velocity to approval.

The Three Tiers of Declined Leads:

- The Hard Decline: Fundamentally unviable due to deep credit impairments or income shortages that no 24-month horizon can fix.

- The Market Victim: Sufficient income, but property price outpaced their savings or the 3% APRA buffer killed the loan-to-income ratio.

- The “Borderline” Borrower: High-earners with “messy” discretionary profiles—BNPL usage, high credit card limits, and lifestyle creep that can be remediated.

Tier 3 is where your future settlements live. By identifying these clients at the point of inquiry, you stop discarding leads you’ve already paid for in marketing acquisition costs.

Step 2: Designing the 24-Month Roadmap

Once identified, the client needs more than a “call me when you save more.” They need a mathematical roadmap. This is where the broker transitions from a transaction manager to a financial coach.

Your job is to provide the client with the specific levers to pull to change this equation. For “Tom,” our target broker, this means giving the client a checklist of closures.

“Look, based on the current 3% serviceability buffer, we aren’t at the ‘Yes’ stage today. However, your fundamentals are strong. If we reduce your credit card limits from $30k to zero and demonstrate a 6-month track record of zero BNPL usage, the math shifts. I’m putting you on our 12-month ‘Path to Approval’ program.”

Step 3: Automating the Shadow Pipeline

You cannot manually manage a 24-month pipeline. It will collapse under the weight of your current deals. Use your CRM to trigger quarterly “Shadow Reassessments.”

| Timeline | Action Item | CRM Trigger |

|---|---|---|

| Month 3 | Confirm Credit Limit Closures | Automated SMS / Document Portal Upload |

| Month 6 | Review Living Expense Trends | Automated Bank Statement Fetch (Yodlee/Illion) |

| Month 12 | Policy Review | Broker Task: Check against updated Lender serviceability |

| Month 18+ | Pre-Qualification Re-run | Direct Phone Appointment |

Step 4: The Compliance Edge (BID)

In the evolving regulatory environment, documenting a long-term “Borderline” journey is a massive compliance win. It demonstrates that you are acting in the client’s **Best Interest** by providing a pathway to homeownership that other brokers or direct-to-bank channels simply ignore.

Checklist for Implementation:

- Audit last 12 months of declined leads for “Borderline” profiles.

- Update CRM stages to include “Pipeline – Rehabilitation”.

- Draft 3 standardized email templates for quarterly check-ins.

- Source a document portal that allows clients to upload savings progress.

{kind=link}