Too Busy to Read? We’ve Got You.

Get this blog post’s insights delivered in a quick audio format — all in under 10 minutes.

This audio version covers: Hiring Your First Broker Support Role: What to Outsource, What to Keep, and How to Structure It Without Payroll Tax Risk

Hiring Your First Broker Support Role: What to Outsource, What to Keep, and How to Structure It Without Payroll Tax Risk

The Australian mortgage broking industry in 2026 is defined by record success and structural fragility. With brokers capturing nearly 77% of the residential market, the operational burden has reached a tipping point. For solo operators, scaling beyond the plateau requires delegation—but the NSW payroll tax controversy has fundamentally altered the risk of hiring.[1, 2]

The “settlement ceiling” for a solo broker typically manifests at three to four loans per month, yet the demands of the Best Interests Duty (BID) require an investment of 15 to 20 hours per file.[3, 4] To scale, brokers must hire; but doing so incorrectly invites scrutiny from revenue offices.[1, 5]

Step 1: The Payroll Tax Crisis

The 2024 Loan Market decision established that the relationship between an aggregator and its brokers often constitutes a “relevant contract”.[6, 2] If a broker engages a support person incorrectly, they may be deemed an employer, triggering back-dated tax liabilities.

| Jurisdiction | 2025-26 Threshold | Standard Rate | Risk Factor |

|---|---|---|---|

| New South Wales | $1,200,000 | 5.45% | Aggressive CPN 016 enforcement [1] |

| Victoria | $1,000,000 | 4.85% (Metro) | Phased threshold reduction [7, 8] |

| Queensland | $1,300,000 | 4.75% | 180-day “business need” rule [7, 9] |

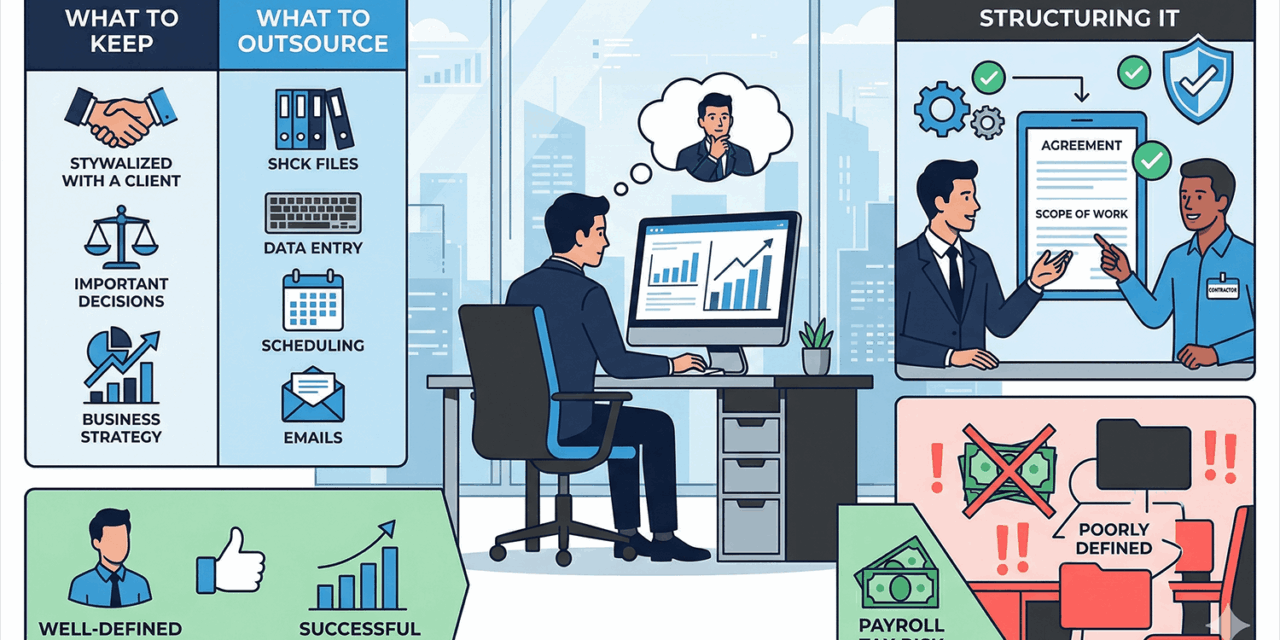

Step 2: Structuring for Exemptions

To mitigate risk, brokers should align their first hire with one of three primary exemptions: the “Two-or-More Persons” rule, the “90-Day” rule, or the “Public Service” exemption.[1]

The Two-or-More Persons Rule: A contract is exempt if the support person (the contractor) engages at least one other person to perform a significant portion of the work.[1] Hiring a processing firm is safer than a single solo virtual assistant.[10, 11]

The 90-Day Exemption Formula

If you only need seasonal support, the 90-day exemption applies. If you lack timesheets, Revenue NSW accepts the “Replacement Method” [10, 12]:

(A = Industry hourly rate; B = 7.6 hours; C = 120% loading; D = 90 days)

Step 3: ASIC Compliance Boundaries

While payroll tax is a fiscal risk, ASIC is a licensing risk. Support staff must strictly avoid “Credit Assistance”.[13, 11]

Task Separation Guide

- Support (Permitted): Data entry, document collation, ordering valuations, and follow-ups.[11]

- Broker (Mandatory): Final product recommendation, presenting options, and explaining the “Why” behind a choice.[11, 14]

Step 4: ROI – Local vs. Offshore

The ROI of the first hire is driven by settlement velocity. An offshore assistant often costs 60-70% less than a local hire.[15]

| Category | Local Hire (Mid-Level) | Offshore Hire (Processor) |

|---|---|---|

| Monthly Base Cost | $5,400 – $6,700 | $2,200 – $2,800 |

| Total Monthly (incl. Super/Ins) | $8,000 – $10,000 | Included in Service Fee |

| ROI (8 extra loans/mo) | Lower (Break-even: 5 loans) | ~560% (Break-even: 1.2 loans) |

*Data based on 2025-2026 industry benchmarks.[15]

Step 5: The 2026 Tech Stack

Support staff in 2026 must be workflow managers, not just data entry clerks. Tools like Salestrekker 2.0 and Cynario Policy AI allow staff to research lender policy in real-time within the client file. Brokers using advanced marketing and automation recorded 156% higher settlement volumes.[16]

Disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. Mortgage brokers should consult with a qualified professional regarding state-specific payroll tax and ASIC obligations.

{kind=link}